Purchasing a home for the first time is a monumental milestone for most people and mortgage life insurance protection can provide piece of mind so loved ones can stay in the home in the event of a premature death. When you peel back the onion most “mortgage protection” is a level term life insurance product for the borrower’s loan amount. The home is one of the largest purchases people make which means the mortgage is typically people’s largest financial obligation. Mentally it is an exciting and stretching time for people with new emotions emerging, especially with the bombardment of mortgage protection letters in the mailbox which can make someone really consider their own mortality and how it effects those they love. People begin to realize the assurance of paying the mortgage loan is based on their health and ability to work. Life insurance provides money to pay off the mortgage balance if the insured (typically homeowner) dies prematurely and can also provide money in the event of a qualifying disability, terminal, chronic, or critical illness. With other types of insurance the policyholder can also receive all their premiums back at the end of the term period or utilize cash value in the policy to pay off their mortgage early. Maintaining adequate insurance coverage will help your loved ones keep the home should the unexpected happen.

[youtube id=”8OcUeqgiAAI”]

Mortgage Protection Insurance

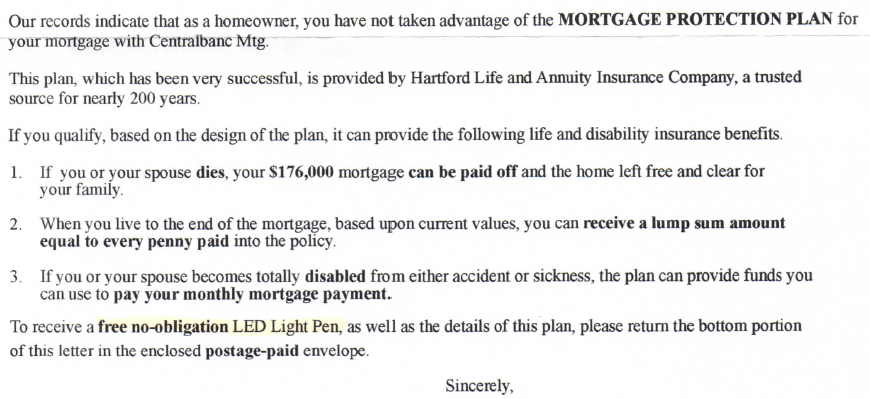

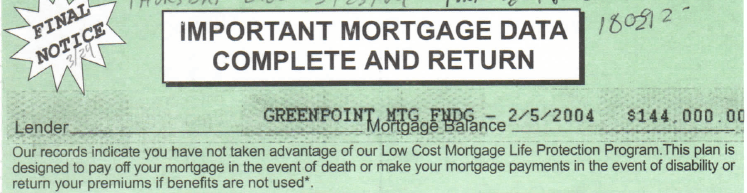

Whenever someone purchases a home it is public record with the county and multiple marketing companies gather or buy this data in order to promote mortgage life protection programs. These mail houses send out millions of letters per year which are intentionally camouflaged to look like they are coming from the lender. Almost always the marketing companies will package the envelopes and letters with the lender’s name, loan amount, and loan date, portraying the lender is the one promoting the program. Some marketing companies get aggressive and even use terminology like “foreclosure protection program” or say “final notice” on the envelopes. Other times the marketing companies try to incentivize the homeowner with a gift, like a “LED Light Pen”. Here are examples of mortgage protection plan mailers:

Mortgage Protection Insurance Companies

In today’s era very few lenders actually endorse or offer mortgage protection programs, but it was not always this way. Back in 1960’s, 1970’s, and early 1980’s mortgage lenders partnered with insurance companies and people could actually include the insurance premium into their monthly mortgage payment. The problem began when lenders started selling off loans and insurance companies where not getting notified of the changes which meant beneficiaries where not correct. Life insurance companies began paying death benefits to wrong lenders, ultimately delaying the process and leaving families in a pinch at the worst time possible. Today, it is better to name the beneficiary directly and have the premium taken electronically out of a personal checking account, this way the owner can be assured their loved ones will have adequate cash to pay off the mortgage balance or make loan payments. Now days most people have their bills electronically coming out of one account anyway, therefore the convenience of it being included in the mortgage payment is old-fashioned and you would be hard pressed to find a lending company that provides this.

In the past almost all mortgage protection insurance was decreasing benefit life insurance, which meant based on the interest rate and mortgage amortization schedule, the insurance company would pay off the remaining balance of the loan. The premium for decreasing term was typically level, meaning the monthly premium stayed the same even though the death benefit decreased each year. Decreasing term was based on old mortality rates and when insurance companies updated cost of insurance, level term life insurance rates became less expensive than decreasing term, which means people can pay less money and have their death benefit stay level and not decrease. This has created a lot of confusion for people who have purchased mortgage protection in the past and were looking for a similar program because almost all the life insurance companies have stopped offering decreasing term life insurance in order to stay competitive with other insurance carriers. The bottom line in today’s age is that mortgage protection insurance is level term life insurance.

Mortgage Protection Insurance Quotes

People should analyze the correct amount of life insurance they should have, factoring the loan amount they owe into the total amount of life insurance needed. The cheapest way to purchase life insurance is to take out a level term life insurance policy, ensuring the correct amount of death benefit for the right period of time. It is usually cheaper to pay for one low cost term life insurance policy with the correct death benefit because every policy has a policy fee. For example, if a person has three term policies equaling 1,000,000, they are paying three different policy fees (usually around $65), rather than having one term life insurance policy which would reduce two policy fees. One should establish the correct amount of life insurance by combining their immediate life insurance needs with their ongoing life insurance needs, then work with an independent life insurance producer who is appointed with several companies. If you would like to speak with someone at our office or generate term life insurance quotes online, without any personal information, please visit http://www.pacificinsurancegroup.com/

Return of premium term life insurance is also commonly marketed with mortgage protection. The concept is if nothing happens and the owner does not die or accelerate any living benefits at the end of a fifteen, twenty, or thirty year period, the owner gets all their premiums back. It is around fifty percent more expensive to add the return of premium rider to the policy but it guarantees the owner gets all the money back as long as premiums are paid the entire time. One caveat with return of premium term life insurance is the policyholder usually has to request their money back; the insurance company with not automatically send a check back to the owner. The reason insurance companies do not typically automatically send the money back to the owner is because it would terminate the policy and the coverage. Since the return of premium term policy is guaranteed renewable, the premiums are guaranteed to stay the same for a period of time such as thirty years and then the policy turns into an annual renewable term policy. If a person happened to be in bad health near the end of the term period it could be wise to keep paying the additional premium in order to keep the death benefit coverage in place and not request to receive their premiums back. If the owner no longer needs life insurance, canceling the policy and receiving all their money back could be a great option.

Another concept around mortgage protection is to utilize a permanent life insurance policy such as whole life or universal life in order to accelerate paying off your mortgage early. Instead of paying additional mortgage payments to the lender consider purchasing a permanent life insurance policy which provides the death benefit in the event of an unexpected death or illness, as well as building a cash value which grows tax-deferred and can be used to pay off the mortgage when the cash value reaches the amount owed on the loan. An advantage to utilizing permanent life insurance over paying additional premiums to the lender is the fact that the cash value in the permanent life insurance policy can be accessed without having to go through a refinancing process. Another advantage to building cash value in the permanent life insurance policy is flexibility for the future. If a person decides they would like to use the policy for estate liquidity, or to potentially supplement their retirement tax-free, they will have multiple options.

Mortgage Protection Life Insurance

Mortgage protection plans can also have a disability income benefit which typically provides a monthly benefit close to a person’s mortgage for certain time periods such as two years. The downside to most disability income attached to mortgage protection is the definition of disability is closer to social security’s definition and qualifying for benefits is fairly difficult. Small monthly benefits capped around $2,000 can be another disadvantage with disability income coverage under a mortgage protection policy. Most of the time a person is better off going with a standalone disability income policy with an easier definition to qualify for benefits. It is also important to understand how much total disability coverage a person has through their work because a person can only be covered for so much benefit. Before someone starts paying extra premiums to include disability income on their mortgage protection policy it is wise to make sure they can actually receive the benefit.

Mortgage protection programs are often times marketed as being “non-medical” or “simplified” from an underwriting standpoint. The non-medical terminology can be confusing because a lot of people think this refers to guaranteed issue, which is definitely not the case. Non-medical means the applicant does not have to meet with a paramedical examiner and give blood, urine, or exam, but the insurance companies still check with the Medical Information Bureau (M.I.B.) in order to background an applicant’s health. Just because the marketing mailer says non-medical, it does not mean the insurance company has to offer the applicant insurance. Non-medical terminology applies to insurance companies offering life insurance as long as there is nothing adverse on the MIB or life application. Typically insurance companies will pool the risk classification into standard non-tobacco and standard tobacco ratings and eliminate preferred health classifications. Non-medically underwritten life policies are not a good deal for people in good health because they will most likely pay significantly more for a non-medical policy. If an applicant is in good health and willing to prove it by giving a blood and urine sample, they can end up paying ¼ the price of a non-medical life insurance policy because they will most likely receive a preferred or super preferred rating. A lot of insurance agents begin their career in the mortgage life insurance protection market and are brainwashed by their up-line that non-medical insurance is quick, premiums are higher, and the agent gets paid faster.

At Pacific Insurance Group we have been helping people with their insurance needs since 2000 and we always put our clients’ well being first. We have worked with a lot of people who started out wanting information about mortgage protection and discovered a better solution. After reading the brochures and understanding the definitions, most people come to the realization that a combination of term life insurance and sometimes a standalone disability income policy can be a better solution at a lower price. Typically people adjust or replace their current term life insurance coverage in order to get the correct amount of life insurance. If you or someone you know is looking for more information about mortgage protection, life insurance, disability income or annuities, email or call our office at 425-246-4222.